Life insurance gives you peace of mind, knowing that your loved ones won’t have to deal with financial hardship after your death. It provides a payout to your beneficiaries that they can use for whatever they choose, such as funeral costs, debts, mortgages, children’s college tuition, and more.

It also pays off your medical expenses. But how do you get the best life insurance policy? Click the www.lifeinsuranceupstate.com to learn more.

Many people are uncomfortable thinking about life insurance, but it is one of the best investments you can make for yourself and your loved ones. A life insurance policy provides a financial safety net for your family after you die, giving them a lump sum of money that they can use to pay expenses or meet other needs. This can help your loved ones maintain their standard of living, pay off debts, or provide for their children’s education.

The money from a life insurance policy can also replace lost income in the event of your death. You can purchase additional riders to increase your coverage, or even cover expenses related to specific events such as critical illness or terminal illness. In addition, the money from a life insurance policy is typically not subject to taxes, providing your beneficiaries with a greater financial benefit.

There are different types of life insurance policies, which can be tailored to fit your unique circumstances. However, before purchasing a policy, it’s important to understand what each type of life insurance covers and how it works. You should also consider how much coverage you need and what your family’s current finances look like.

You can get a general idea of the cost of a life insurance policy by using an online calculator or speaking to an agent. Factors that influence the cost of a policy include your age, gender, and health status. Additionally, if you smoke, the price of your policy may be higher. You can also find out if there are any discounts available for smokers or check to see if you’re eligible for a group plan through your employer.

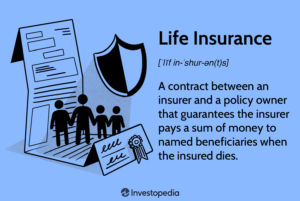

A life insurance policy is a contract between an individual and the insurer. In exchange for regular premium payments, the insurer promises to pay a specified amount, known as the death benefit, to the beneficiary upon the individual’s death. The death benefit can be used to pay funeral costs, settle outstanding debts, and cover other financial obligations. You can also purchase a policy with a fixed term, which guarantees that the beneficiary will receive a set amount of money if you die within the specified period.

It pays a death benefit

When someone dies, their beneficiaries receive a payout from a life insurance policy. These payments can be used however the beneficiary chooses, such as covering funeral costs or putting children through college. This is a great way to make sure your family’s finances are protected in case of the unexpected. Here’s how it works:

Beneficiaries must file a claim with the insurance company that holds the deceased person’s life insurance policy or annuity. The process can take 30 to 60 days depending on the circumstances and how quickly the beneficiaries provide necessary documentation. The insurance company will need to verify the beneficiaries’ identity and relationship to the deceased. It will also need to know the insured’s policy number and policy details, including death benefits and payment preferences.

The type of payout depends on the type of life insurance policy. There are several types, each with different premiums and benefits. Some policies offer additional features, called riders, that can increase the death benefit or provide living benefits to the insured while they are still alive. For example, an accidental death rider could significantly increase the payout if you died from an accident. Other riders include accelerated death benefits, which let you access the death benefit early if you have a terminal illness.

There are several factors that influence how much a life insurance policy will pay to your beneficiaries, including the length of the term and the amount paid in premiums. The longer the term, the higher the premiums. Some insurance companies also require a medical exam before they issue a policy.

A beneficiary can choose a lump-sum payout or a life income annuity, which pays out a fixed sum over the rest of the insured’s lifetime. The payout amounts are based on the insured’s estimated life expectancy, and longer life expectancies lead to smaller payments. This option may work well for a beneficiary who is uncomfortable managing a large sum of money and prefers lifetime income.

If the beneficiary is not able to manage the payout amount, they can borrow against the policy’s cash value. This loan must be repaid before the insured dies, or it will be deducted from the death benefit.

It pays for funeral expenses

Life insurance is one way to ensure that your loved ones will have enough money to pay for your funeral and burial expenses. A policy can cover a range of expenses, including funeral home services, cremation fees, and burial merchandise. There are many options for life insurance, but the best one for you will depend on your preferences and budget. You can also choose a preneed funeral policy to save time and money by setting aside funds for your final arrangements.

One type of life insurance that can help with funeral costs is term life insurance. This type of policy provides a fixed amount of coverage for a certain period of time, and it is often less expensive than whole life insurance. However, there are some drawbacks to this type of policy, including the possibility that it will not pay out if you die outside the policy term.

Another option is to set aside money in a savings account for funeral expenses. This can be helpful, but it’s important to remember that these funds will only be available if your loved ones can find the money when you pass away. It’s also possible that the savings won’t be enough to cover all your funeral expenses, especially if funeral prices rise in the future.

Burial insurance, which is often referred to as final expense insurance, is a type of life insurance that pays a death benefit to your beneficiaries when you die. This type of insurance is designed to provide coverage for end-of-life expenses, such as funeral costs and unpaid medical bills. This type of policy is typically marketed to older people, and it doesn’t require a medical exam.

Other types of life insurance, such as whole and universal life insurance, also offer a cash value component that can be used for funeral expenses. However, these policies typically cost more than term life insurance, and they may not pay out a lump sum immediately upon death. If you want to use your life insurance to pay for funeral expenses, it’s important to contact the insurer right away so they can process your claim.

It pays off debts

Life insurance is often purchased as a way to provide for a family in the event of an unexpected death. But it also has the potential to help with debts, and many policies allow policyowners to borrow against their accumulated cash value for this purpose. This option may help to pay off a debt and save the policyholder hundreds of dollars in interest. However, this type of borrowing is not for everyone and should only be considered with some forethought and research.

Debt weighs on countless individuals every day, damaging their financial well-being and degrading their mental health. In addition to reducing the stress of surviving family members, debt can prevent people from enjoying their life and putting off major purchases. However, if you are currently carrying substantial debt, life insurance can offer a solution. By using a policy loan to pay off your debt, you can free yourself from this burden while still alive and give your family a solid financial safety net.

The process of taking a policy loan is quick and easy and does not require credit score checks or justification. However, it is important to note that the loan amount will be deducted from your policy’s death benefit when you die. This is one of the reasons it is important to make sure that you have a policy with significant cash value before deciding to take out a loan.

To determine if you can borrow against your life insurance, consider your current debts, how much income your family would need to replace after you’re gone, and the costs of funeral expenses, home repairs, and children’s college tuition. Then, add up all of these expenses to calculate your required death benefit. It is also important to remember that not all types of life insurance are eligible for a policy loan. Only permanent life insurance that accrues a cash value is eligible to be used as loan collateral. Term life insurance, on the other hand, does not accrue cash value and therefore cannot be borrowed against.

Borrowing against your life insurance is a simple and convenient way to relieve your debts, but it is not a good idea for everyone. You must carefully consider the pros and cons of this financing solution, as well as your financial circumstances and goals.